All Categories

Featured

Table of Contents

Annuities offer tax-deferred growth. When you gain interest in an annuity, you usually do not need to report those incomes and pay earnings tax obligation on the profits yearly. You can maintain funds in your account to reinvest and compound. Development in your annuity is insulated from personal revenue tax obligations. At some point, you will certainly have to pay income taxes on withdrawals from an annuity agreement.

While this is a review of annuity taxes, seek advice from a tax obligation expert prior to you make any type of decisions. Multi-year guaranteed annuities. When you have an annuity, there are a number of details that can influence the taxes of withdrawals and revenue payments you get. If you put pre-tax cash right into a specific retired life account (INDIVIDUAL RETIREMENT ACCOUNT) or 401(k), you pay taxes on withdrawals, and this holds true if you money an annuity with pre-tax cash

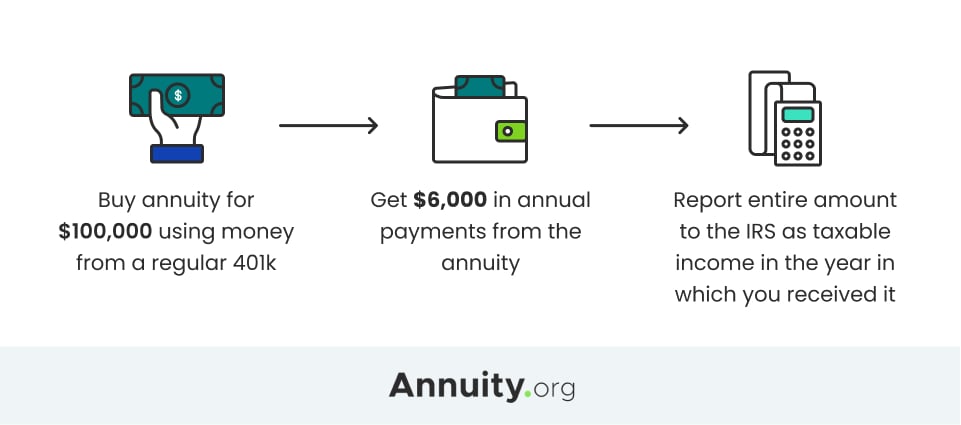

If you have at the very least $10,000 of revenues in your annuity, the whole $10,000 is dealt with as revenue, and would commonly be tired as ordinary revenue. After you wear down the earnings in your account, you obtain a tax-free return of your initial lump sum. If you transform your funds into a guaranteed stream of income payments by annuitizing, those repayments are divided into taxable portions and tax-free sections.

Each repayment returns a portion of the money that has actually already been strained and a section of interest, which is taxable. As an example, if you obtain $1,000 monthly, $800 of each repayment could be tax-free, while the staying $200 is gross income. At some point, if you outlive your statistically determined life span, the whole amount of each repayment might end up being taxed.

Given that the annuity would have been funded with after-tax money, you would not owe taxes on this when taken out. Because it is identified as a Roth, you can additionally possibly make tax-free withdrawals of the development from your account. To do so, you must adhere to numerous IRS guidelines. Generally, you have to wait up until a minimum of age 59 1/2 to withdraw profits from your account, and your Roth must be open for a minimum of five years.

Still, the various other attributes of an annuity may surpass earnings tax treatment. Annuities can be tools for delaying and taking care of taxes.

What taxes are due on inherited Annuity Death Benefits

If there are any kind of charges for underreporting the earnings, you could be able to ask for a waiver of fines, however the rate of interest normally can not be waived. You might be able to prepare a layaway plan with the IRS (Joint and survivor annuities). As Critter-3 claimed, a neighborhood professional may be able to aid with this, but that would likely cause a little bit of extra cost

The initial annuity agreement owner should consist of a survivor benefit arrangement and call a recipient - Annuity rates. There are different tax consequences for spouses vs non-spouse beneficiaries. Any kind of beneficiary can pick to take an one-time lump-sum payout, however, this features a hefty tax problem. Annuity beneficiaries are not limited to people.

Fixed-Period Annuity A fixed-period, or period-certain, annuity makes sure payments to you for a particular size of time. Repayments might last 10, 15 or 20 years. If you pass away throughout this time around, your chosen beneficiary gets any kind of continuing to be payments. Life Annuity As the name recommends, a life annuity guarantees you repayments for the remainder of your life.

Inheritance taxes on Lifetime Annuities

If your contract includes a survivor benefit, staying annuity settlements are paid to your beneficiary in either a round figure or a series of payments. You can pick someone to obtain all the offered funds or a number of individuals to obtain a portion of continuing to be funds. You can additionally pick a nonprofit company as your beneficiary, or a count on developed as component of your estate plan.

Doing so permits you to maintain the exact same options as the original owner, consisting of the annuity's tax-deferred condition. You will additionally have the ability to get remaining funds as a stream of settlements rather than a swelling amount. Non-spouses can likewise acquire annuity payments. They can not alter the terms of the agreement and will only have access to the assigned funds laid out in the initial annuity agreement.

There are three main methods beneficiaries can get acquired annuity repayments. Lump-Sum Circulation A lump-sum distribution enables the beneficiary to receive the contract's whole staying value as a single settlement. Nonqualified-Stretch Arrangement This annuity contract clause allows a beneficiary to get settlements for the remainder of his/her life.

In this situation, tax obligations are owed on the entire distinction in between what the initial proprietor paid for the annuity and the fatality benefit. The lump sum is taxed at common income tax prices.

Spreading out settlements out over a longer period is one way to stay clear of a big tax obligation bite. If you make withdrawals over a five-year duration, you will owe tax obligations only on the boosted value of the section that is withdrawn in that year. It is additionally much less most likely to push you into a much higher tax bracket.

Tax consequences of inheriting a Lifetime Annuities

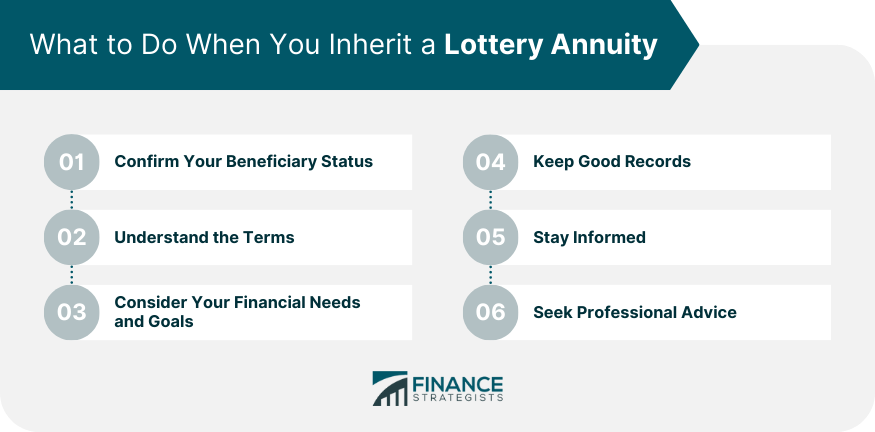

This uses the least tax obligation direct exposure but likewise takes the longest time to obtain all the cash. Annuity income. If you have actually acquired an annuity, you typically have to choose about your fatality advantage swiftly. Decisions concerning just how you desire to receive the cash are frequently final and can't be transformed later on

An acquired annuity is a monetary product that allows the beneficiary of an annuity agreement to continue obtaining repayments after the annuitant's fatality. Acquired annuities are usually used to give earnings for loved ones after the fatality of the primary income producer in a household. There are 2 sorts of acquired annuities: Immediate inherited annuities start paying right away.

Guaranteed Annuities inheritance tax rules

Deferred inherited annuities permit the beneficiary to wait till a later date to start receiving settlements. The very best thing to do with an acquired annuity depends upon your economic situation and requirements. An instant acquired annuity might be the most effective choice if you require instant income. On the various other hand, if you can wait a while before beginning to obtain payments, a deferred inherited annuity may be a better selection. Immediate annuities.

It is necessary to talk to an economic expert prior to making any type of choices regarding an acquired annuity, as they can assist you establish what is best for your specific scenarios. There are a few risks to take into consideration before purchasing an acquired annuity. Initially, you ought to recognize that the federal government does not assure acquired annuities like other retired life items.

Taxes on inherited Annuity Death Benefits payouts

Second, acquired annuities are commonly complicated financial items, making them hard to comprehend. Speaking with a economic advisor before spending in an acquired annuity is vital to guarantee you totally recognize the threats entailed. There is always the threat that the worth of the annuity can go down, which would minimize the amount of cash you get in payments.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices A Closer Look at Fixed Interest Annuity Vs Variable Investment Annuity What Is Immediate Fixed Annuity Vs Variable Annuity? Benefits of Choosing the Right Financi

Analyzing Fixed Vs Variable Annuity Pros And Cons A Closer Look at Fixed Vs Variable Annuities What Is the Best Retirement Option? Advantages and Disadvantages of Different Retirement Plans Why Choosi

Highlighting What Is A Variable Annuity Vs A Fixed Annuity A Closer Look at Fixed Income Annuity Vs Variable Growth Annuity Defining Choosing Between Fixed Annuity And Variable Annuity Pros and Cons o

More

Latest Posts